Market-Makers Make Markets

Rethinking Supply and Demand

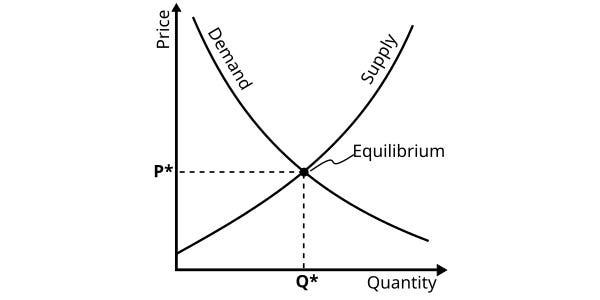

Economists tend to imagine commodity markets as a pair of intersecting supply and demand curves. The price that clears the market is the price where buyers want to buy the same quantity that sellers want to sell.

"Supply and demand" by SilverStar, modified by Alex Howlett, is licensed under CC BY 2.5.

{kind=link}

When the balance between buyers and sellers becomes mismatched, we might expect the price to adjust to clear the market. However, too much price volatility would interfere with the market. The good news is that if the mismatch between supply and demand is temporary, someone can profit by buying when everyone is selling and vice versa.

All that is needed to make it realistic is to introduce intermediary traders, neither final buyers nor sellers, who on occasion may either buy or sell.

(Hicks 1989, 9)

The intermediaries "make" the market by ensuring there will always be buyers and sellers and that the price will stay reasonably stable. They supply market liquidity by absorbing supply and demand mismatches into their own inventories.

In his Money and Banking lectures (2012) and elsewhere, Perry Mehrling describes market-makers using Jack Treynor's (1987) model of the securities dealer.

In the above diagram, dealers quote buy and sell prices (the inside spread), adjusting those prices as their inventories change; more inventory leads to lower prices.

[T]he money view has two foundational elements: banking as a payments system, and banking as a market-making system. The constraint to settle payments daily, the so called “survival constraint”, provides essential discipline to encourage agents throughout the economy to line up cash inflows and outflows in time, and to make provision to fill gaps by borrowing or lending in short term money markets. In this frame, the money rate of interest appears as the price of relaxing the survival constraint by borrowing. Alternatively, one can meet a deficit by selling some financial asset, into more or less liquid markets. In the money view, the price in those asset markets is understood as arising from the economics of the dealer function, an “inside” bid-ask spread quoted by profit-seeking market-makers who offer to counterparties the facility to move from money (means of payment) to financial assets, and vice versa, for a price.

(Mehrling 2023, 3)

Prices come from markets made by market-makers providing liquidity. And liquidity lets people meet their payment commitments to satisfy their survival constraint.

The traditional view that market price is, at least in some way, determined by an equation of demand and supply had now to be given up. If demand and supply are interpreted, as had formerly seemed to be sufficient, as flow demands and supplies coming from outsiders, it is no longer true that there is any tendency, over any particular period, for them to be equalized; a difference between them, if it were not too large, could be matched by a change in stocks [inventories].

(Hicks 1989, 11)

Clip Length: 7:53 (2017 Lec 3, 57:01–1:04:54)

In the lectures, Mehrling adapts the Treynor model to funding markets, too. It turns out that interest rates and funding liquidity also come from market-makers making markets.

References

Hicks, John. 1989. A Market Theory of Money. Oxford: Clarendon Press.

Mehrling, Perry. 2012. "Economics of Money and Banking." Online course. Coursera. Accessed 2015–2025. https://www.coursera.org/learn/money-banking

Mehrling, Perry. 2017. "Lecture 3: Fundamentals of the Money View." Warsaw School of Economics, recorded October 13, 2017. Video of lecture, 1:27:49. https://youtu.be/XzMXkJDksrE

Mehrling, Perry. 2023. "Exorbitant Privilege? On the Rise (and Rise) of the Global Dollar System." Institute for New Economic Thinking Working Paper Series No. 198. https://doi.org/10.36687/inetwp198.

Treynor, Jack L. 1987. "The Economics of the Dealer Function." Financial Analysts Journal 43 (6): 27–34. https://doi.org/10.2469/faj.v43.n6.27.

Survival constraint is a very clever and apt name for your blog and a very important financial principal in general. Mehrling is of course one of the most competent and clear speakers on the mechanics of money and banking.

The inside-outside spread visualization is an incredibly useful graphic for understanding market making. The idea that market makers can reliably profit using a markup or discount, despite market volatility, is simple enough, but I have always struggled to visualize it. Thanks for sharing that.

I also talk about "survival" in my rate disparity book, but in the context of assessing interest equilibriums, as there is a mismatch between expected returns and realized post-hoc returns:

https://ratedisparity.com/wiki2/index.php/Rate_Disparity_Book

I am still working on making that book better and simpler and clearer, as I tried to tackle a lot and took a lot of speculative and complex ideas.